Autumn 2026

Our quarterly briefing

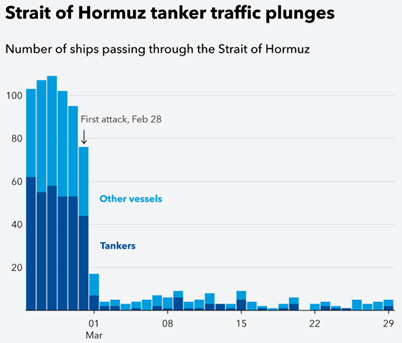

So far, the central economic question for 2026 has been how long the Strait of Hormuz will be closed. The situation is fast moving, volatile, and fragile.

At the time of writing, a ceasefire agreement hangs in balance as the United States (US) administration negotiates with Iran to enabling the reopening of the Strait of Hormuz as soon as possible. However, that does not necessarily mean an immediate return to peacetime or the complete reopening for maritime traffic, with uncertainty persisting. Assuming a resolution of the conflict in April or May (in some form) – which seems probable but is in no way guaranteed – the questions become whether, and when, Iran agrees to an end to the war (depending on its policy towards Israel), how fast maritime traffic can recover, across the Strait and more widely, and if the resolution is sustainable.

In times of crisis and high uncertainty, the accuracy of economic forecasting is weakened, with results hingeing primarily on assumptions. Our baseline assumption is an April or May resolution to the conflict, and a gradual recovery of traffic in the Strait over the following weeks and months.

The alternative scenario is a continuation of the war, perhaps with “boots on the ground” in Iran in some form. The prospects of this alternative scenario are difficult to model because, frankly, of how dire they would be for the global economy and stability. The worst-case scenario is an ensuing cascade of refined oil export restrictions across the world if supply tightens to unsustainable levels (i.e., if global reserves start running out). Such a grim cascade scenario could literally ‘seize up’ the global economy. Diplomatic efforts and cooperation have avoided such systemic restrictions to date, thankfully, and we do not deem this scenario likely at present.

However, a plausible ‘middle ground’ scenario, largely undiscussed as yet, is the gradual passage of selected tankers through the Strait while the war between Iran and the coalition continues. There are already signs of certain cargo carrying vessels (friendly to Iran in one way or another) passing through the Strait, along with a “toll” system being established. While it is unlikely volumes would recover to pre-war levels in this scenario, as Iran would otherwise lose its leverage, it would make up for some of the supply shock to selected Asian economies (China in particular). The question is whether New Zealand will sit on the right side of this scenario, if it eventuates, with our refined fuel imports largely coming from Singapore and South Korea.

Nevertheless, assuming an April or May resolution, stagflation – the combination of inflation and slower or stagnating growth – best characterises the outlook for the global and New Zealand economies. The initial oil supply shock and higher petrol prices will raise inflation, while economic growth in New Zealand will slow through 2026, relative to the excepted recovery prior to the conflict.

Our main question from the outset has been – why aren’t oil prices higher and global financial markets sharply correcting, given the scale of the oil supply shock?

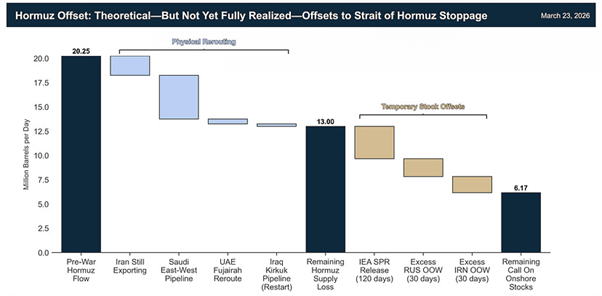

Since the first attacks by the US and Israel, and Iran’s retaliation, oil prices have ranged from $90 to $120 per barrel, depending on the type of crude. We would expect higher prices for a total closure of the Strait of Hormuz, through which about 20 percent of global oil trade flows. Arguably there are offsets, mainly alternative Gulf pipelines, the International Energy Agency (IEA) global reserves release, and the removal of sanctions on both Russian and Iranian crude oil already in transit.

For context, in the early days of the Russia-Ukraine conflict the feared supply shock was estimated at three million barrels per day, or about three percent of global trade, and prices swiftly rose to above $100 per barrel. Even accounting for all of the available practical and theoretical offsets to the Strait of Hormuz closure, both rerouting and temporary offsets, the shock to global markets would still be twice that of the Russia-Ukraine conflict (three percent compared to six percent of global supply).

There are two main potential reasons why oil prices did not shoot up instantly to around $150, or higher, per barrel. Firstly, markets appear to have been pricing in an April or May resolution from the beginning. Secondly, the US and Israeli administrations have been jawboning markets, by repeatedly making statements that the conflict is nearing its end, to prevent oil prices rising too fast and equities market correcting too violently. Arguably, Iran’s objectives were precisely the opposite; to find the market’s “breaking point” and apply pressure on the US administration leading into the mid-terms (although without breaking Asian economies relying on Gulf crude). Indeed, this conflict is taking place kinetically across the Gulf, as well as simultaneously in global financial markets.

Markets have been relatively accepting of the coalition’s public interventions so far. But our view is that markets will gradually fully price-in the economic implications of the shock to the global economy as the effectiveness of jawboning gradually erodes and wanes. This will result in oil prices remaining elevated and equities suffering. The “physical” oil market will lead the “financial and speculative” oil market higher. New Zealand’s Kiwisaver balances will be collateral damage in the process.

Examining the channels of impact

The impact on the global economy and supply chains is related to the duration and severity of the conflict, along with the continuation of the strikes on critical infrastructure throughout the Middle East. There are both immediate and long-term structural consequences, however, regardless of when the conflict is resolved and the Strait is opened.

Some impacts are materialising quickly in the economy. Elevated energy prices are the most obvious and widely experienced. Supply chains are another transmission channel for the impacts of this conflict, with increased freight and insurance costs from rerouting ships, plus longer delivery times for a range of commodities, not just oil. Expect this to put further pressure on prices.

To examine some of the wider impacts from the Middle East conflict, we analyse the implications for oil, and how these flow through to key areas such as agriculture, fertiliser, and travel. The full range of implications are broad and stretch across economies, from transport (a key impact), to the supply of plastics (a niche impact).

Oil – petrol, diesel, and fuel oil

Regardless of the resolution to the Middle East conflict, even if we expect an April or May resolution, we can confidently expect oil prices to remain at a structurally higher level over the long-term. This will reflect damage to crucial energy infrastructure in the region taking time to repair (i.e., regional productive capacity has been diminished) and countries looking to (re)build reserves following the exposure of this shock.

This negative supply shock in parallel will lead to elevated prices globally. It is expected that the global flow of oil will take months before becoming “normalised” again, whatever “normal” may look like in the aftermath of this defining event. A likely consequence could be that, in the long-term, countries will aim to reduce their risk exposure.

“The war in the Middle East is creating the largest supply disruption in the history of the global oil market.” (IEA, 2026)

The disruption to the global oil market is already severe. The immediate impact of this disruption materialised quickly in New Zealand through higher petrol and diesel prices at the pump. In particular, diesel prices have increased significantly following the breakout of the war. This has strongly impacted our agriculture, construction, transport, and manufacturing sectors, as well as consumer use, which is likely to be captured in some of the preceding sectors. This a troubling sign as the Ministry for Business, Innovation and Employment (MBIE) acknowledges diesel as our “most important fuel by volume and strategic value.”

Under an April or May resolution scenario our current assumption, although far from certain, is that we anticipate oil prices remaining elevated around $100 per barrel for at least a year. Importantly, we do not see New Zealand import supply becoming an issue under this scenario. Rather, prices will be the central issue. Over the long-term, countries may look to diversify their exposure to such impacts given what will likely be a fragile and volatile resolution.

Some countries, particularly in Asia, which are seriously at risk as they are both large importers of unrefined oil and exporters of refined oil, are already implementing emergency measures in response to the crisis. Such measures include urging (or even mandating) lower consumer energy demand, transport and fuel restrictions, limiting public travel, and requiring remote work where possible. We do not anticipate New Zealand “running out” of fuel. However, it is likely that in a prolonged conflict prices will become so steep that some measure of demand destruction will occur.

At present, New Zealand is operating under phase one of the National Fuel Plan which, in a broad sense, involves monitoring the situation with no restrictions in place. This is more or less a “business as usual” approach. An extended conflict will increase the likelihood of shifting to phases where measures to manage both demand and supply come into play, more in line with what many countries are already doing. An April or May resolution scenario implies that we may be likely remain in phase one, however, in any alternative scenario New Zealand will shift to higher phases.

Agriculture – a major consumer of diesel and fertiliser in New Zealand

New Zealand’s agriculture sector is explicitly impacted in two direct ways: as a major consumer of diesel and as an importer and user of fertiliser.

Diesel use in the agricultural sector is widespread and is across much of the production chain from diesel-fuelled utes used by farmers, to heavy machinery and equipment. The sector accounts for around ten percent of diesel use in the country. Because of this widespread use and dependence, the ongoing crisis has revealed a critical economic exposure in the agriculture sector. For a large portion of diesel users in the sector, there are no alternatives. Heavy machinery, equipment, and fleet vehicles cannot use substitutes for diesel.

The supply of fertiliser is another issue for the agricultural sector that has been exposed due to the conflict. Around one third of the global supply of fertiliser passes through the Strait and New Zealand’s urea (a key nitrogen fertiliser) supply is heavily concentrated in the Gulf. At present, this is placing pressure on prices, but an extended conflict will begin to put pressure on supply, which is an entirely different challenge. Fertiliser has become so embedded in agricultural production worldwide that a dramatic shift in the level of global supply would cause valid food security concerns.

We can expect that the combination of higher diesel and fertiliser prices will increase pressure on farm margins as higher input costs weigh on revenue. This will be compounded by increased logistics and transport costs. In the short-term, farmers will absorb the costs, but over time this will be passed on to consumers. Under an April or May resolution scenario, the extent of this pass-through will be contained, but prices will remain elevated for at least a year.

The alternative scenario of a prolonged conflict, which is not our base case, is more worrying for New Zealand’s agriculture sector. For fertiliser, the consequences vary but would be severe for particularly dependent industries, such as arable production. Stocking rates or yields can be expected to decline, and production will follow.

Tourism

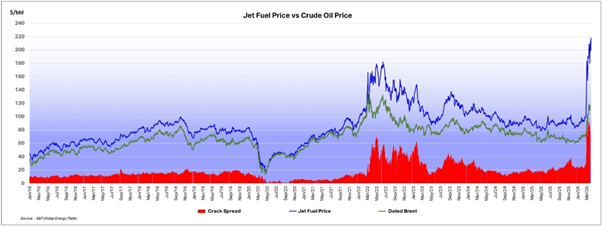

The effects of higher energy prices are already impacting New Zealand’s connectivity to the rest of the world, but are also being felt domestically. The price of crude oil per barrel has dominated many of the headlines but jet fuel prices have increased beyond $200 per barrel, doubling within a matter of weeks.

In response airlines, including Air New Zealand, are already cutting the number of flights and raising airfares. This is impacting both international and domestic airlines and flights. As a relatively large land mass that is geographically dispersed, regional connectivity is critical to the functioning of the New Zealand economy and society more generally as well. Rural communities are dependent upon flights for access to healthcare, business, and education.

On the international front the immediate impact is on tourism, which is a valuable component of economic activity in New Zealand. Flight disruptions, increased airfares, and general consumer reluctance will impact international visitors’ numbers. This is added pressure to the tourism sector that has only recently begun recovering from the persistent impacts of COVID-19. On the other hand, we can expect some New Zealanders to holiday at home because of these effects.

Broader impacts from the Strait closure

It is likely that the implications of this conflict will be geopolitically defining for years to come. This includes Iran’s control over the Strait, with obvious consequences for the Gulf Cooperation Council (GCC), but potentially more broadly for NATO and the Ukraine-Russia conflict as well. The economic fallout, at a minimum, will span weeks and months throughout 2026, with some lingering effects being evident for years.

Global crude oil prices are expected to be structurally $10 to $20 higher per barrel because of an additional “risk premium” for the remainder of 2026 at least, even with the Strait gradually reopening. Global oil supply chains have been entirely disrupted. Weeks, or more likely months, will be needed for the oil trade to normalise back to pre-conflict flows across the world, while some infrastructure has been destroyed.

We have previously noted the slow moving, but deteriorating, sovereign debt positions across the developed world throughout 2025, particularly in the US, Europe, and Japan. Global interest rates have risen as a result of the stagflationary shock from the Middle East conflict. The weight of debt on governments and households will be felt more intensely throughout 2026 (at least). The New Zealand government’s fiscal position is itself being closely monitored by rating agencies.

Further broader consideration includes the impact on the artificial intelligence industry. Coincidentally, the boom in energy hungry artificial intelligence data centres is now taking place in the midst of the largest oil supply shock in history and an energy crunch. In addition, Helium supply is also being impacted. While the US is relatively more insulated and energy self-sufficient, the outlook for AI generally is dampened by the current energy situation.

Finally, while the conflict in the Middle East is front and centre, the US economy, which leads the global economic cycle, was showing signs of deceleration coming into 2026. Its slowing employment growth, and emerging issues in the private credit sector, although relatively contained so far may flow through to the broader economy. Altogether, 2026 isn’t looking promising so far.

The BERL take

The policy debate focus to date has been on the government’s immediate response and efforts to secure supply, along with ongoing monitoring of fuel imports and reserves. We expect our fuel import supply chains to continue to remain resilient, with an April or May resolution as our baseline assumption.

While understandably somewhat narrow in the immediate instance, the policy response will need to progressively expand to account for the likely wider effects of the closure of the Strait of Hormuz. This will be similar to the COVID-19 pandemic response which initially focused on lockdowns, and then moved to supporting the economy through border closures.

The central question for the government to consider is whether this is yet another delay to recovery and growth, or does it call for a rethink of its economic strategy?

As its third Budget and the election period approaches, the government will consider whether the key tenets of its economic strategy (concisely summarised, perhaps unfairly, as “lower spend and interest rates”, “back to basics and surplus”, and “going for growth”) will still hold in light of yet another economic shock. Evidently 2026 is not looking promising. The New Zealand economy will be both experiencing the impacts and digesting the fallout of the shock, even after the Strait opens, through most of this year.

Has the conflict in the Middle East, following the Liberation Day tariff shock last year and a series of economic disappointments, given the death blow to the government’s approach? It will largely depend on how long the Strait is closed but, at a minimum, some revisions or augmentations of the government’s strategy would arguably be required. Growth is expected to yet again disappoint, cost of living will return as a central theme, and global interest rates are already rising.

This shock is not primarily a test of short-term policy responses, but of whether New Zealand is capable of governing its economic trajectory beyond electoral cycles.

The first step is getting consensus around the right diagnosis. Is this shock another “speed bump” on the way to recovery and growth, or is this a “new world” calling for a different approach, or is it somewhere in between? The overall strategic policy mindset and options fall out of this initial diagnosis, which Cabinet and the governing coalition need to discuss and agree upon.

A rupture calls for a medium-term economic trajectory strategy and plan

“We are in the midst of a rupture, not a transition” – Prime Minister of Canada, Mark Carney, speech at Davos 2026

A fitting place to provide our first BERL take for 2026 is to pick up where we left off in 2025.

We concluded our Summer QEB with Minister Willis’s closing comment for HYEFU 2025. She expressed her desire for an “upside economy surprise” for 2026, after what had been a series of disappointing forecast revisions until then. Our parting line for the year was that we argued, instead, for a more structured and deliberate plan for improving our economic trajectory.

Our argument is not to suggest that the government should have predicted the conflict in the Middle East. Rather, it is that the domestic and global conditions now need to be recognised for what they are. These conditions have been, and are, calling for the development and maintenance of a consistent medium-term macro and microeconomic policy framework that is attuned to the realities of our environment.

Throughout 2025, our view has been that “economic uncertainty is here to stay”. Our Spring 2025 QEB concluded that – “The line between shocks and structural changes is blurring. […] On this basis, it would be practical for the government to attune its approach to the level and persistence of global economic uncertainty.”

This requires a change in mindset, where shocks unfolding more frequently since the beginning of the decade, and the COVID-19 pandemic, are not mere deviations from the baseline and plan, or “bumps in the road” (as initially dubbed by the Prime Minister). Instead, our view is that they are features, not bugs, of the economic environment we are in. Anecdotally, this difference in mindset was at its starkest in our engagement with the recent delegation of Singaporean politicians and officials in Wellington.

What does this mean in practice? What should the government do?

Coming back to what is now the largest energy shock in modern history, the simplified framework through which to understand the impact of an oil supply shock of this scale is that it is inflationary first but destroys demand and growth second. Because monetary policy operates on a lag of 12 to 18 months, the Reserve Bank of New Zealand (RBNZ) needs to weigh both effects on this timeline.

Currently, and assuming an April or May resolution, our view is that crude oil prices oscillating above $100 per barrel will sit somewhat uncomfortably. They are high enough to increase inflation but they are not so high, as yet, that they will destroy demand significantly. Most central banks are currently in a “wait and see” mode. Although they may need to react quickly if the conflict endures, and choose which direction to take (with loosening and tightening finely balanced), acknowledging the RBNZ's relative hawkish stance in their latest announcement.

On the fiscal side, the simplified policy framework is to: a) provide support to the most vulnerable and impacted households, while b) not adding fuel (pun unintended) to the initial inflation shock caused by higher petrol prices, and c) continue to act in a fiscally prudent fashion as global interest rates rise.

We are in the early stages of this economic crisis, and there is an array of topics to be traversed on what it means for New Zealand and the government. Our constructive prescription at this early stage is consistent with our call for a medium-term economic strategy laid out in our recent article “Beyond the pump”. In short, the response to the shock needs to be designed in such a way that it is consistent with longer-term objectives for the economy as we eventually come out of the crisis.

“First, governments and businesses try to cushion the blow, with temporary and targeted support for those under the most pressure. Second, they position the economy for recovery, lining up the investments and initiatives that support a rebound. Third, they can reset and restructure, using the shock to reduce vulnerability and set the economy on a more resilient path.”

The challenge, but more importantly the opportunity, is to make those three phases work together. The crisis becomes an opportunity to leverage the initial response in a way that lays the ground for a credible way of setting, maintaining, and adjusting a medium‑term economic trajectory that survives beyond three‑year electoral cycles.

Economic strategies, elections, and consensus

However, there are some complications. There isn’t a medium-term economic strategy to speak of through which to see the prism of this situation, and design the response to the crisis. The complication is not that New Zealand is in an election year, but that our economic strategy is structurally reset every election year. In an environment of frequent, overlapping shocks, this governance rhythm is increasingly misaligned with the realities of the global economy.

Because our economic management mindset is not strategically prepared for this situation, we will likely be building the plane as we fly it through 2026. Taking the example of energy policy, arguably the most front and centre policy area for 2026 and the general election, is revealing:

- Following a lack of supply investments (in part due to lack of political consensus in the first place), a dry year in 2024 caused wholesale electricity prices to spike, straining the manufacturing sector in particular, This was followed by the US tariffs in 2025 and the subsequent ripple effect through the global economy).

- The action taken was to commission a structural review of the sector and markets. The Government rejected the main strategic recommendations, instead opting to pursue an LNG terminal.

- In light of the conflict in the Middle East and the spike in natural gas prices, the LNG terminal policy is now under review and may be cancelled.

- Labour’s election pledge is to repeal the LNG terminal policy unless it is materially progressed. Arguably, the incentive is now for National to progress it regardless, or in a diminished form, to lock it in.

After a full three-year parliamentary cycle, it wouldn’t be an exaggeration to say that we risk being back to where we started on structural energy policies. Whether full ownership, or splitting the gentailers, ever becomes the alternative policy platform, they themselves would be likely to require a consensus to be enduring.

New Zealand is a small open economy at the bottom of the South Pacific operating in a more complex world.

It is not realistic to close the productivity gap with more productive economies over the next few years and decade, with unstable and inconsistent structural policies that do not provide a pathway for the economy over the medium-term.

In addition, more frequent shocks, from different sources ranging from climate to geopolitical conflicts, must now start to be built into our policy settings by planning for the medium-term.

Strategic economic resilience and autonomy (SERA)

Since early 2026, even prior to the conflict, we have in our engagements promoted the idea of a SERA plan, or strategic economic resilience and autonomy plan. To dispel predictable critics, we are not advocating autarky.

To not dance around it, a SERA plan would include a policy discussion on the role of the government in vertical settings, and with the most ambitious iteration, although not necessarily the only, being a form of industry policy. Notably, based on our understanding of the Australian policy environment and engagement with officials, industrial policy is making a gradual albeit sustained return in Canberra.

A SERA plan is not a policy programme, nor a substitute for political debate. It is an organising framework for economic decision making that sets durable objectives, constraints, and priorities within which governments of different stripes can operate.

Our prescription for a medium-term economic strategy, applicable to a potential SERA plan, has remained the same:

- Define roles and responsibilities - Define the respective roles and responsibilities between government, business, and households in adjusting to structural shocks. The public and private sectors would ideally be working more closely together to agree on the respective roles and responsibilities.

- Set a path - Set out medium-term macro and microeconomic pathways. Balance ‘horizontal settings’ with ‘vertical’ policies to develop priority areas of the economy or sectors for structural change. Energy, intersecting with climate and transport, will be a primary policy focus area over the next year.

- Identify value-for-money - Identify targeted areas where government intervention provides compelling value-for-money and the returns justify the cost of intervening (i.e., neutral to the crown’s balance sheet over the medium-term).

- Be consistent - Establish a consensus view on the desired outlook for key aspects of the economy. We have publicly commented on, and are contributing to, the development of tools and institutional solutions to developing enduring cross-party political consensus.

- Internalise structural shocks and prepare to react - Understand the blurring of cyclical economic shocks and structural changes as geopolitical, climate, economic, and other shocks and vulnerabilities increasingly intersect. Recognise the persistent uncertainty and be prepared to react accordingly. Refrain from expecting the “coast to be clear” (like after the Liberation Day tariffs) once the Strait of Hormuz eventually reopens, or broader normalisation on the other side of the Trump presidency. For example, risks around the Taiwan Strait remain regardless, while Cuba looms as the US’s next potential country of focus.

Parting thoughts

Ultimately, the most important question raised by the closure of the Strait of Hormuz is not how quickly global supply chains normalise, but whether New Zealand can move from governing its economy in episodes to governing its trajectory deliberately.

In a world where shocks are persistent rather than exceptional, economic resilience becomes less about reactive policy settings and more about institutional capability, strategic clarity, and political consensus that extends beyond electoral cycles.

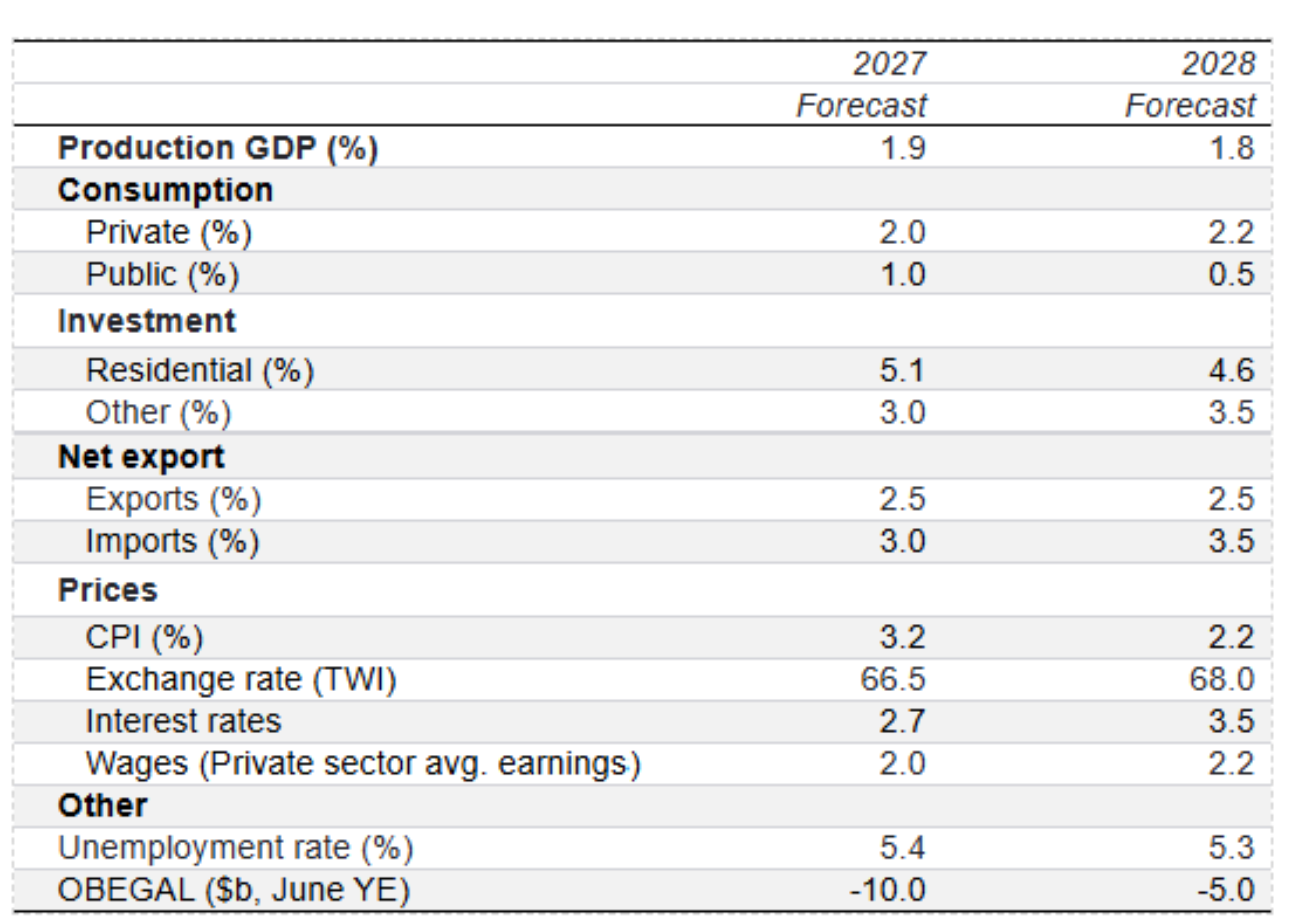

BERL economic forecasts

BERL Forecasts

Source: BERL analysis

*All forecasts are to March years, except OBEGAL.